South African Department Of Energy IPP Office

South African Department Of Energy IPP Office

The Department of Energy (DoE), National Treasury (NT) and the Development Bank of Southern Africa (DBSA) established the IPPPP Unit for the specific purpose of delivering on the IPP procurement objectives. The activities of the office are in accordance with the capacity allocated to renewable energy and non-renewable generation in the Integrated Resource Plan (IRP) 2010; subsequent ministerial determinations and DoE support service requirements.

The IPPPP activities continue to evolve in order to effectively respond to the planning and development needs in the current energy context. As an example, the IPPPP Office has been requested to coordinate the development of the Gas Utilisation Master Plan (GUMP) that will in turn guide the procurement of the required gas capacity as per the IRP 2010.

|

www.ipp-projects.co.za |

|

Bylsbridge Office Park, Building 9, Cnr Jean and Olievenhoutbosch Ave, Centurion |

| S 25.53’8.977” E 28.12’7.003” |

|

| +27 87 351 3000 | |

|

info@ipp-projects.co.za |

Introduction to the IPP procurement programme

The National Development Plan (NDP) identifies the need for South Africa to invest in a strong network of economic infrastructure designed to support the country’s medium- and long-term economic and social objectives. Energy infrastructure is a critical component that underpins economic activity and growth across the country; it needs to be robust and extensive enough to meet industrial, commercial and household needs.

The NDP requires the development of 10,000 MWs additional electricity capacity to be established by 2025 against the 2013 baseline of 44,000 MWs.

The (policy adjusted) Integrated Resource Plan (IRP) 2010 developed the preferred energy mix with which to meet the electricity needs over a 20 year planning horizon to 2030.

In line with the national commitment to transition to a low carbon economy, 17,800 MW of the 2030 target are expected to be from renewable energy sources, with 5,000 MW to be operational by 2019 and a further 2,000 MW (i.e. combined 7,000 MW) operational by 2020.

Planning requirements further include capacity to supply for base load and medium term risk mitigation (MTRM) plans.

In May 2011, the Department of Energy (DoE) gazetted the Electricity Regulations on New Generation Capacity (New Generation Regulations) under the Electricity Regulation Act (ERA).

The ERA and Regulations enable the Minister of Energy (in consultation with NERSA) to determine what new capacity is required. Ministerial determinations give effect to components of the planning framework of the IRP, as they become relevant.

2,500 MW

designated from coal-fired plants

800 MW

of cogeneration under the MTRM plan

3,126 MW

of Gas-fired power plants (2,652 MW base load + 474 MW MTRM)

2,609 MW

of imported hydro

A significant share of the new electricity capacity will be developed and produced by Independent Power Producers (IPPs).

The introduction of private sector generation offers multiple benefits. It will contribute greatly to the diversification of both the supply and nature of energy production, assist in the introduction of new skills and in new investment into the industry, and enable the benchmarking of performance and pricing.

The New Generation Regulations establish rules and guidelines that are applicable to the undertaking of an IPP Bid Programme and the procurement of an IPP for new generation capacity.

These guidelines include:

- compliance with the IRP;

- the acceptance of a standardised power purchase agreement (PPA);

- a preference for a plant location that contributes to grid stabilisation and mitigates against transmission losses;

- and a preference for a plant technology and location that contributes to local economic development.

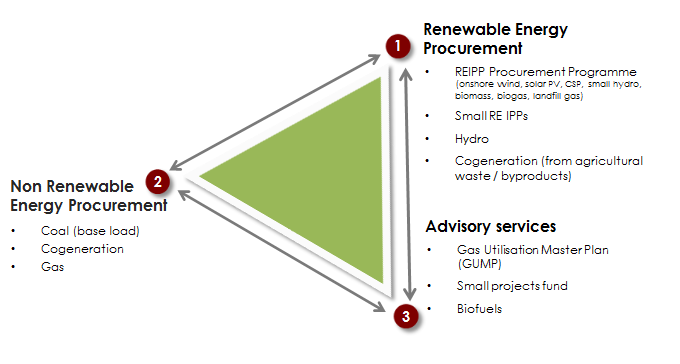

The Independent Power Producers Procurement Programme (IPPPP) Office and mandate

The Department of Energy (DoE), National Treasury (NT) and the Development Bank of Southern Africa (DBSA) established the IPPPP Unit for the specific purpose of delivering on the IPP procurement objectives.

In November 2010 the DoE and NT entered into a Memorandum of Agreement (MoA) with the DBSA to provide the necessary support to implement the IPPPP and establish the IPPPP Office.

The activities of the office are in accordance with the capacity allocated to renewable energy and non-renewable generation in the Integrated Resource Plan (IRP) 2010; subsequent ministerial determinations and DoE support service requirements.

The IPPPP Office provides the following services:

- Professional advisory services;

- Procurement management services;

- Monitoring, evaluation and contract management services (as from 7 July 2014) – with contract period of 20 years.

It has been applauded for effectively avoiding the quicksand of laborious administrative arrangements, without undermining the quality or transparency of the programme.

The IPPPP partnership is funded by a Project Development Facility (PDF) financed through bid registration fees payable by all bidders and the Development Fee paid by selected bidders.

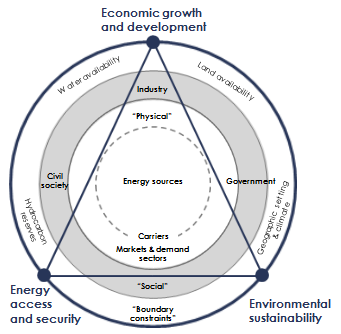

Increasingly, a sound, comprehensive energy strategy is structured as a triangle with the three sides denoting, respectively: promoting economic development, providing energy security and access while achieving environmental sustainability.

South Africa’s current electricity development strategy aims to achieve a greater balance between these three aspects, focusing on achieving a balanced energy mix to include more gas and renewables.

An appropriate approach to development of a sustainable energy portfolio has to take cognizance of how new development and capacity delivers against the imperatives of the energy triangle.

Economic growth and electricity consumption have outpaced power system capacity building in South Africa in the preceding two decades. As a result the country has been experiencing severe electricity supply constraints since 2008. The 2008/9 global economic recession slowed down economic activity and, as a consequence, electricity demand, providing a temporary reprieve. But, after a slower than anticipated economic recovery, 2014 again saw the power system stressed to its limits. To maintain system stability, a schedule of rolling black outs have been instituted, but with dire implications for the stressed economy.

It is foreseen that electricity supply will continue to be highly constrained for at least the next five years as the build programme catches up with demand. The Department of Energy, in collaboration with key stakeholders, are looking at various options to alleviate the crisis, including through increasing and accelerating the participation of IPPs in the energy sector. This situation is likely to reshape the IPPPP portfolio.

As part of mitigating the shortfall, both supply and demand management solutions that can rapidly deliver reliable capacity and reduce or shift demand cost effectively and timeously, will be prioritised for immediate implementation.

It is envisaged that the IPPPP will continue to provide a flexible procurement service to the Department for a responsive and effective reply to the urgent power infrastructure development needs of the country.